Decentralised finance (DeFi) aims at democratising finance by replacing centralized financial institutions with direct, peer-to-peer relationships for improving the availability and efficiency of the financial services. DeFi mainly uses blockchain technology, cryptocurrencies and smart contracts to manage wide variants of financial transactions.[1]

The below figure enlists certain financial transactions and how they are managed in DeFi vis-a-vis traditional finance:

Source: Alexandra Born et al., Decentralised finance – a new unregulated non-bank system? (https://www.ecb.europa.eu/pub/financial-stability/macroprudential-bulletin/focus/2022/html/ecb.mpbu202207_focus1.en.html)

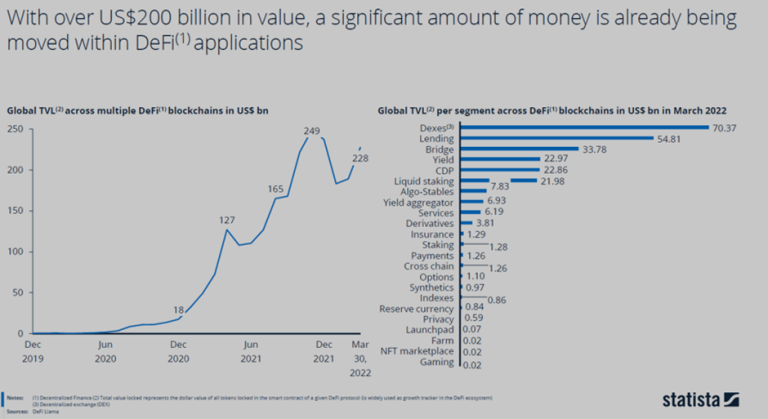

The below image shows some statistics around total value locked in DeFi as of March 2022.

Source: Digital Economy Compass 2022 – Chapter 1, The ascent of the crypto economy (Statista)

The purpose of this blog is to discuss tax implications on certain DeFi transactions. (covered in next section)

Several countries around the world have already laid down certain guidelines for taxation of DeFi transactions. Some are in the process of laying down the guidelines. For example: UK released public consultation in relation to the taxation of DeFi transactions for lending and skating of the cryptoassets.

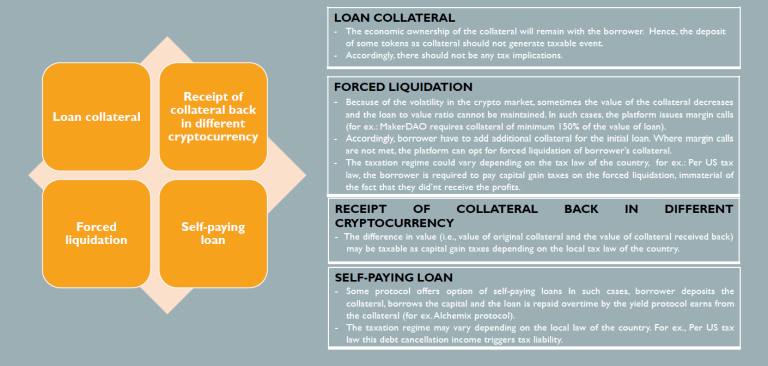

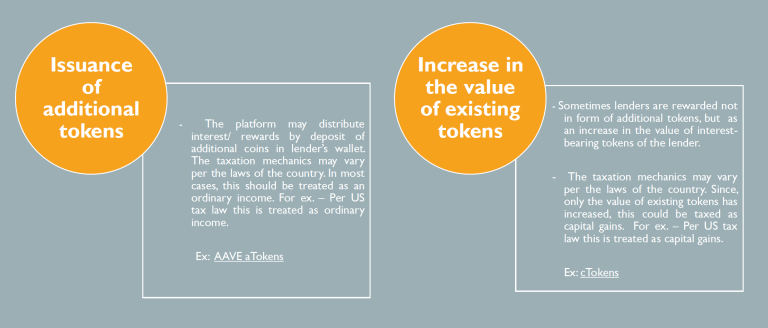

Certain DeFi transactions are discussed below (this is not an exhaustive list of transactions):

The determination of tax implications in case of DeFi transactions should be based on facts, circumstances and actual nature of the transactions. The taxation mechanics for the same DeFi transaction could vary across countries based on the local tax laws of the countries.

In all:

[1] https://pelaghiaslaw.com/2022/03/24/decentralized-finance-defi-the-european-regulatory-perspective/

[2] https://tokentax.co/blog/defi-tax-guide; https://cryptotaxcalculator.io/blog/the-ultimate-defi-tax-guide/

For slides refer below :

Skip to PDF content

The views in all sections are personal views of the author.