In part 2 of the series, I have discussed Article 24(1) which deals with Nationality non-discrimination in detail. In this part, I will discuss Article 24(2) dealing with the stateless person

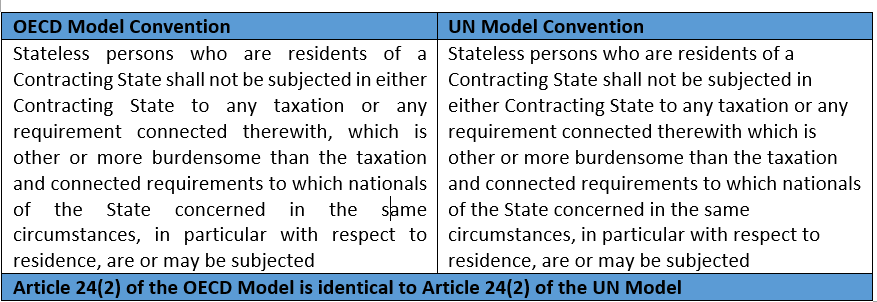

As mentioned earlier, Paragraph 2 of Article 24 of the OECD model convention extends the benefit of the non-discrimination clause to stateless person who are residents of one of the contracting states.

Thus, Article 24(2) applies if the following conditions are satisfied –

Note – Indian treaties do not contain a similar paragraph in its tax treaties. The reason may be because the arrangements deal with ‘Resident of a contracting state’ and irrespective of whether a ‘resident’ is a ‘national’ or ‘stateless’. Only India- Norway tax treaty has a similar clause.

Important texts from OECD commentary in relation to Article 24(2) –

Para 28 – The purpose of paragraph 2 is to limit the scope of the clause concerning equality of treatment with nationals of a Contracting State solely to stateless persons who are residents of that or of the other Contracting State.

Para 31 – It is possible that in the future certain States will take exception to the provisions of paragraph 2 as being too liberal insofar as they entitle stateless persons who are residents of one State to claim equality of treatment not only in the other State but also in their State of residence and thus benefit in particular in the latter from the provisions of double taxation conventions concluded by it with third States…………

The views in all sections are personal views of the author.