The purpose of this series is to have a discussion on the non-discrimination clause of the bilateral tax treaties considering the issues surrounding it along with the Indian judicial pronouncements

Article 24 of the OECD Model Convention deals with non-discrimination. Article 24 is a special rule providing for the avoidance of discrimination against nationals or residents of another contracting state. However, the non-discrimination obligations of Article 24 apply only if nationals or residents of two states are comparably situated. For example – for a non-discrimination article to apply, they should either carry on the same activities or be in the same circumstances.

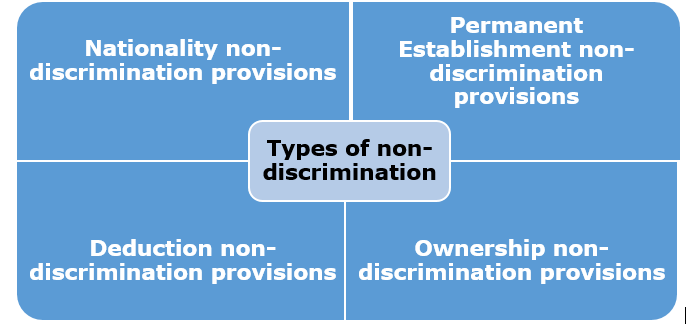

The essence of a non-discrimination article is to prevent unfair taxation as distinct from preventing double taxation. Bird eye view on the types of non-discrimination discussed in the tax treaties –

Overview of the different para’s of Article 24 as enlisted in OECD Model Convention –

- Article 24(1) of the OECD Model Convention deals with Nationality non-discrimination and it states that for purposes of taxation, discrimination on the grounds of nationality is forbidden, and that, subject to reciprocity, the nationals of a Contracting State may not be less favourably treated in the other Contracting State than nationals of the latter state in the same circumstances.

- Article 24(2) of the OECD Model Convention deals with the Non-discrimination for stateless person having nationality and it prevents stateless person resident in a state from being subjected to any taxation or other requirement which is more burdensome than similar requirements with respect to nationals of that state. Per se, Article 24(2) extends the same benefits as Article 24(1) to a stateless person who is a resident of one of the contracting state.

- Article 24(3) of the OECD Model Convention deals with Permanent Establishment (‘PE’) non-discrimination and it states that a PE of an enterprise of State ‘A’ in State ‘B’ shall not be subjected in State ‘B’ to taxation less favourable than the taxation levied on an enterprise of State ‘B’ carrying on the same activities.

- Article 24(4) of the OECD Model Convention deals with deduction Non-discrimination and it states that where a resident of State ‘A’ pays interest, royalties, or other disbursements to a resident of State ‘B’, then, the rules for deductibility of such payments in computing taxable profits of the resident of State ‘A’ should be the same as are applicable in respect of the payments made to another resident of State ‘A’ itself.

- Article 25(5) of the OECD Model Convention deals with ownership non-discrimination and it states that an enterprise in State ‘A’ which is wholly or partly owned or controlled, directly or indirectly by residents of State ‘B’ should not be subjected in State ‘A’ to any taxation or connected requirement which is other or more burdensome than taxation or connected requirement to which another enterprise in State ‘A’, in the same circumstance, is subjected to.

- Article 24(6) of the OECD Model Convention deals with General (taxes covered) and it states that Article 24 is applicable to taxes of every kind and description notwithstanding the provisions of Article 2 (Taxes covered) of the Model Convention.